A balance sheet is a financial statement that provides an overview of a business’s financial position by listing its assets, liabilities, and equity at the end of an accounting period. It is prepared after the trading and profit and loss accounts and is essential for understanding the financial health of a business.

Not-for-Profit Organizations also prepare balance sheets to assess their financial position. Like trade entities, they list assets on the right side and liabilities on the left side. However, instead of capital, a General Fund or Capital Fund is used to account for surplus or deficit adjustments.

Table of Content

- Features of Balance Sheet

- Importance of Balance Sheet

- Purpose of the Balance Sheet

- How to prepare a Balance Sheet?

- Balance Sheet Format

- Reserve in Balance Sheet

- Consolidation of Balance Sheet

- How to Prepare Consolidated Balance Sheet?

Features of a Balance Sheet

The key features of a balance sheet include:

- Final Step in Account Creation: The balance sheet is prepared last in the accounting process.

- Not an Account, but a Statement: It is a statement of the business’s assets and liabilities.

- Two Sides: Assets are recorded on the right-hand side, while liabilities are recorded on the left-hand side.

- Balancing Requirement: Total assets should always equal the total of liabilities and equity.

- Financial Position Snapshot: It shows the financial standing of a business at a specific point in time.

Importance of a Balance Sheet

A balance sheet is a crucial document for businesses and stakeholders alike. Here’s why:

- Stakeholder Insight: Creditors, investors, and other stakeholders use it to assess a company’s financial status.

- Growth Analysis: Comparing balance sheets over multiple periods reveals growth trends.

- Loan Applications: Lenders often require balance sheets to evaluate a company’s creditworthiness.

- Liquidity Assessment: It helps stakeholders evaluate the liquidity position of the business.

- Future Planning: Analyzing a balance sheet can indicate areas for business expansion and potential future expenses.

Purpose of a Balance Sheet

The main purpose of a balance sheet is to reflect a company’s financial condition. It highlights the assets, liabilities, and equity, offering insight into resource allocation and debt levels. Investors and creditors rely on balance sheets to gauge a company’s ability to generate returns. While a balance sheet can be prepared anytime, it is typically created at the end of the financial year for annual financial reporting.

How to Prepare a Balance Sheet

Follow these steps to create a balance sheet:

- Compile a Trial Balance: Start by listing all general ledger account balances.

- Adjust the Trial Balance: Make any necessary adjustments, so the trial balance matches the accounting structure.

- Remove Income Statement Items: Exclude all revenue and expense accounts, leaving only assets, liabilities, and equity.

- Summarize Remaining Accounts: Total the relevant line items, which typically include:

- Assets: Cash, accounts receivable, inventory, fixed assets

- Liabilities: Accounts payable, accrued liabilities, debt

- Equity: Common stock, retained earnings

- Balance the Sheet: Ensure the total assets equal the total of liabilities and stockholders’ equity.

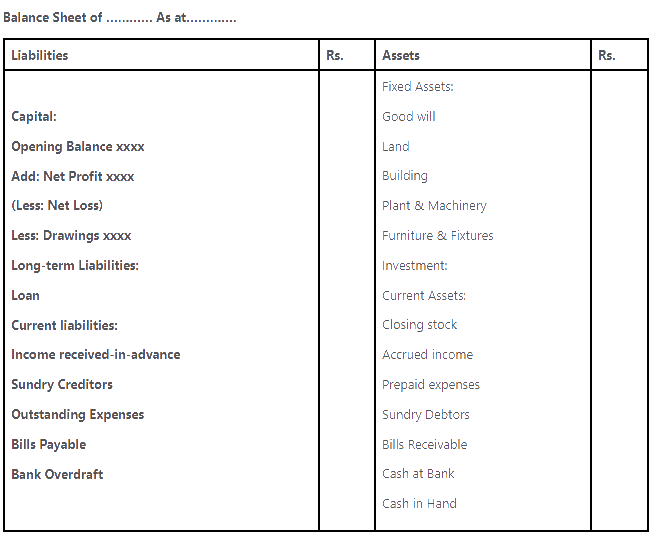

Balance Sheet Format:

The balance sheet of a company will look like the image given below.

What is a Reserve in the Balance Sheet?

A reserve is an amount retained from profits to strengthen a company’s financial position, cover debts, fund expansion, or prepare for specific expenses. Reserves are listed as liabilities on the balance sheet and are important for financial planning. For instance, an insurance company may keep a reserve to ensure sufficient funds to pay out claims. These funds are set aside and not used for other purposes, providing financial security for future obligations.

Consolidation of a Balance Sheet

A consolidated balance sheet combines the assets and liabilities of a parent company and its subsidiaries into a single document. When a company holds a controlling stake of 50% or more in another business, it issues a consolidated statement. This process involves adjusting the values of subsidiary assets to reflect current market value. Importantly, the revenue of the parent company is not added to avoid duplication.

Steps to Prepare a Consolidated Balance Sheet:

- Label the Document: Include the parent company, subsidiary names, and the date.

- Organize Assets, Liabilities, and Equity: Group items under these headings.

- Ensure Consistency: Verify the total assets, liabilities, and equity match with the parent company.

- Adjust for Duplicates: Eliminate duplicate entries across parent and subsidiary accounts.

The above mentioned is the concept that explains ”What is a Balance Sheet and its characteristics” for the Class 12 students. To know more, stay tuned to Eduacademy.