Accounting for Revaluation of Assets and Liabilities upon Partner Retirement or Death

When a partner retires or passes away, it is crucial to reassess certain assets and liabilities that might not have been updated to their current values. Similarly, some liabilities may have been recorded at a value different from the actual obligation owed by the company.

Unrecorded assets and liabilities must be incorporated into the books. When a new partner is admitted, the Revaluation Account is adjusted to determine the total gain or loss based on the reassessed value of assets and liabilities, including any previously unrecorded items. This revaluation amount is then transferred to the capital accounts of all existing partners, including the retiring or deceased partner, according to their profit-sharing ratio.

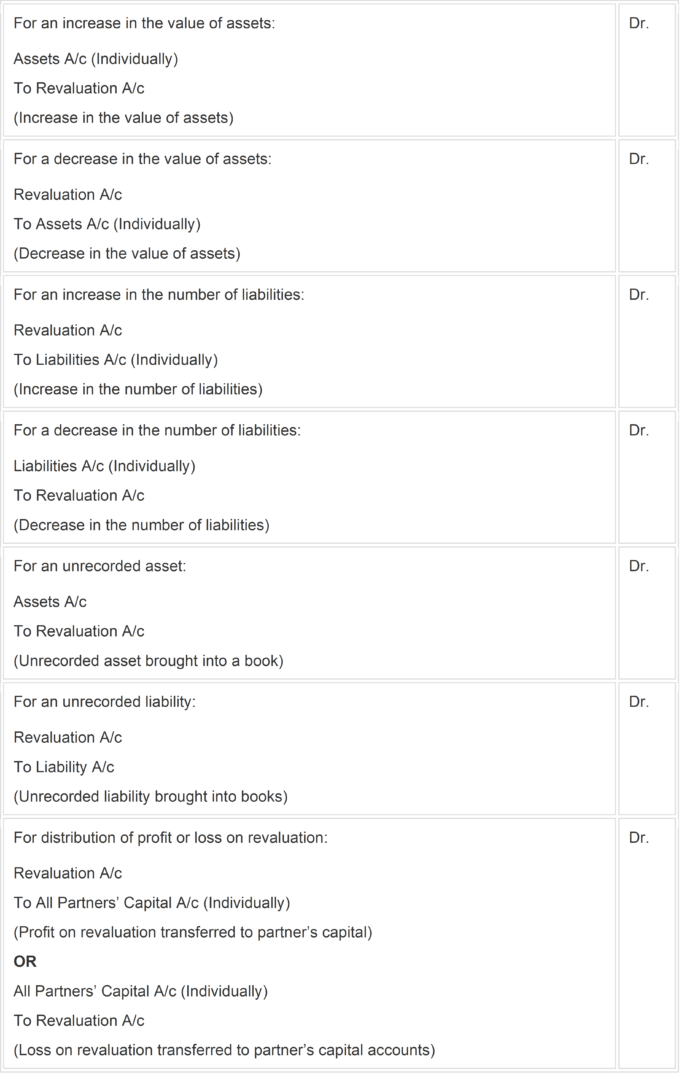

Journal entries to be passed are mentioned below:

(The above mentioned Journal entries are fetched from NCERT website)

This was all about the concept of Adjustment for Revaluation of Assets and Liabilities which is presented in this article for the benefit of Class 12 Commerce students. To learn more, stay tuned to eduacademy.